A rental appraisal is a professional estimate of the rent your property can achieve in the current market, based on comparable properties, local demand, and the specific features of your home. Property managers and licensed appraisers in South Australia use this process to give landlords a defensible, evidence-based rent figure rather than a guess. Getting this number right is the difference between a fully occupied property generating strong returns and one sitting vacant because the rent is set too high or leaving money on the table because it is set too low. This guide covers how rental appraisals work, the methods used, the factors that drive valuations, and how you can use appraisal data to maximise your rental income across the Adelaide market.

What is a rental appraisal and how does it work?

A rental appraisal, also called a market rent assessment in formal property circles, is a structured analysis of what a property should rent for based on current market evidence. The process follows a clear sequence. A property manager or licensed appraiser inspects the property, gathers data on comparable rentals in the area, and applies one or more valuation methods to arrive at a recommended weekly rent figure.

The most widely used method is comparable market analysis. This involves identifying 3 to 5 similar properties recently leased or currently listed within a close radius of your property. Appraisers look at properties with similar bedroom counts, property type, condition, and location. They then adjust the rent figures up or down depending on how your property compares on specific features.

Adjustments always move from the comparable property toward the subject property. If a comparable property has an extra bathroom that yours does not, the comparable rent is adjusted downward to reflect that difference. If your property has a larger garage or a renovated kitchen, the comparable's rent is adjusted upward. This logic keeps the analysis grounded in real differences rather than broad assumptions.

For investment properties, appraisers also apply the income capitalisation approach. This method values the property using NOI divided by the cap rate, where NOI is the net operating income after expenses. Income capitalisation is the most reliable approach for investment analysis because it reflects actual earnings rather than speculative sale prices. A cost approach is occasionally used for unique or newly built properties where comparable data is limited.

Pro Tip: Ask your appraiser which method they weighted most heavily and why. A good appraiser will explain their reasoning clearly. If they cannot, that is a signal to seek a second opinion.

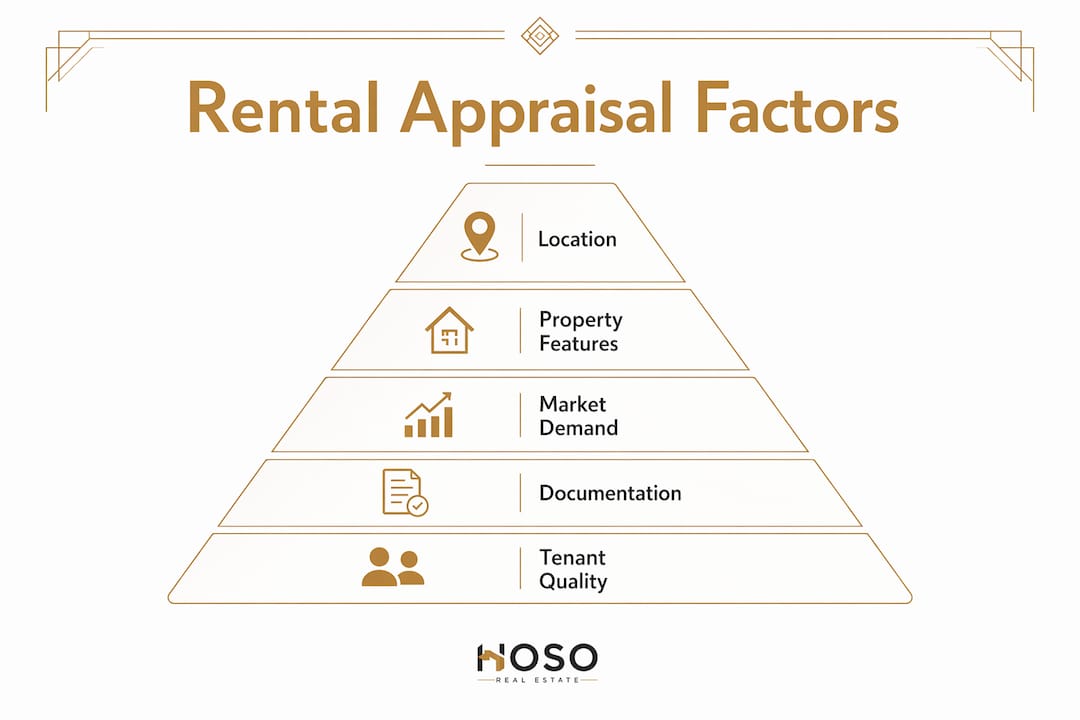

What factors most influence rental appraisal values?

Location is the single strongest driver of rental value in South Australia. Properties in suburbs with strong school zones, reliable public transport, and proximity to the Adelaide CBD command consistently higher rents. Suburbs like Norwood, Unley, and Prospect attract professional tenants willing to pay a premium for lifestyle access. Outer suburbs with new infrastructure investment, such as Mawson Lakes or Seaford, show rising demand as tenant demographics shift.

Property features matter significantly after location. Bedroom count, bathroom count, car parking, outdoor space, air conditioning, and overall condition all affect where your property sits within the local rent range. A well-maintained three-bedroom home in Glenelg will appraise higher than an identical floor plan in poor condition on the same street. Renovations to kitchens and bathrooms typically produce the strongest uplift in appraised rent.

Market supply and demand conditions shape the upper and lower bounds of any appraisal. Conservative rent growth assumptions sit at 2% to 3% annually, with healthy vacancy rates running between 5% and 10%. Adelaide has experienced tighter vacancy than the national average in recent years, which pushes appraised rents upward as competition among tenants increases.

Documentation also affects appraisal accuracy in ways many landlords overlook. Providing rent rolls, leases, and proof of payments gives the appraiser stronger evidence to work with, producing a more defensible figure. Many property owners arrive at an appraisal without this paperwork, which forces the appraiser to rely on generic market estimates rather than property-specific data.

Pro Tip: Compile a simple folder with your current lease, recent rent receipts, and any maintenance records before your appraisal. It takes 20 minutes and meaningfully improves the quality of the report you receive.

What types of rental appraisal reports are there?

Not all rental appraisal reports are the same. The type you need depends on your purpose, whether that is setting a new rent, refinancing, or satisfying a lender's requirements.

-

Rent letter (addendum). A rent letter is the simplest form of rental assessment. It provides a quick indication of market rent without a thorough interior inspection. Rent letters cost less than full appraisals and suit situations where a rough market figure is sufficient, such as an initial investment inquiry.

-

Standard rental appraisal. This is the most common report type for landlords. A standard appraisal costs $200–$400 and typically involves an exterior inspection and comparable market analysis. It is valid for 60–90 days depending on lender requirements. Most property managers in Adelaide provide this as part of their onboarding process.

-

Full narrative appraisal. This is the most detailed report type. It includes an interior inspection, a thorough analysis of all valuation methods, and a written narrative explaining the appraiser's conclusions. Full narrative appraisals cost more and take longer to produce. Lenders commonly require them for mortgage applications, DSCR loans, and refinancing decisions.

The table below summarises the key differences between report types.

| Report type | Inspection level | Typical cost | Validity period | Best use |

|---|---|---|---|---|

| Rent letter | None or limited | Under $100 | Short term | Initial market inquiry |

| Standard appraisal | Exterior only | $200–$400 | 60–90 days | Rent setting, basic lending |

| Full narrative appraisal | Interior and exterior | Above $400 | Lender dependent | Mortgage, refinancing, disputes |

Lenders commonly disregard the actual rent in your lease and instead rely on an independent market rent figure when assessing your borrowing capacity. This makes a credible, up-to-date appraisal report a practical requirement for any landlord planning to refinance or expand their portfolio.

How can property owners use appraisals to maximise rental income?

Accurate appraisal data is the foundation of a sound rental strategy. Setting rent too high extends vacancy periods. Setting it too low erodes your annual return. A current appraisal removes the guesswork and gives you a market-tested figure to work from.

Using multiple valuation methods produces a more balanced and trustworthy result than relying on a single approach. Combining comparable market analysis with income capitalisation gives you both a market perspective and an investment performance perspective. Relying solely on the Gross Rent Multiplier, for example, risks a misleading conclusion because it ignores operating expenses and vacancy.

Regular appraisals are worth scheduling even when you are not changing tenants. The Adelaide rental market moves quickly, and a rent figure from 18 months ago may no longer reflect current conditions. Landlords who review their rental strategy at least annually are better positioned to adjust rents at lease renewal without triggering tenant disputes or vacancy.

Tenant quality also feeds into long-term income performance. A property with a strong tenant screening history and consistent payment records supports a higher appraised rent because it demonstrates reliable income. Appraisers and lenders both take note of tenancy stability when assessing income reliability.

Pro Tip: When your appraisal comes back, ask your property manager to walk you through the comparable properties used. Understanding why those comps were selected tells you exactly what features are driving rent in your area right now.

For a deeper look at how to analyse a rental property deal beyond the appraisal figure, layered investment analysis frameworks are worth reviewing before any major rent or portfolio decision.

Key takeaways

A rental appraisal is the most reliable tool a landlord has for setting rent that is competitive, evidence-based, and aligned with current South Australian market conditions.

| Point | Details |

|---|---|

| Appraisal types vary by purpose | Choose between rent letters, standard appraisals, or full narrative reports based on your specific need. |

| Documentation improves accuracy | Providing leases, rent rolls, and payment records gives appraisers stronger evidence to work with. |

| Multiple methods reduce risk | Combining comparable analysis with income capitalisation produces a more reliable rent figure. |

| Regular reviews protect returns | Schedule appraisals at least annually to keep rent aligned with current Adelaide market conditions. |

| Lenders use market rent, not lease rent | An independent appraisal is required for refinancing, as lenders disregard actual lease figures. |

HOSO's take on rental appraisals

Most landlords treat a rental appraisal as a one-off task they do when a property first hits the market. That is a mistake. The Adelaide rental market has moved considerably over the past few years, and a rent figure set in 2023 or 2024 is unlikely to reflect what the market will bear today.

What I see consistently is landlords undervaluing their properties in suburbs like Prospect, Kurralta Park, and Clarence Gardens because they are working from outdated comparables or a property manager's verbal estimate rather than a formal assessment. A proper appraisal with documented comps changes that conversation entirely.

The other issue is documentation. Landlords who bring their lease, rent roll, and maintenance history to an appraisal get a materially better report. Those who show up empty-handed get a generic estimate that may not hold up under lender scrutiny.

My advice is straightforward. Get a formal appraisal every 12 months. Use it to inform your rent review conversation with your property manager. And if you are refinancing or expanding your portfolio, commission a full narrative appraisal rather than relying on a standard report. The cost difference is minor. The difference in quality and lender acceptance is not.

— HOSO

HOSO Real Estate rental appraisal services for SA landlords

HOSO Real Estate works with Adelaide landlords who want accurate, current rental valuations backed by real market data.

Whether you are setting rent for a new tenancy, preparing for a lease renewal, or planning a refinance, HOSO Real Estate provides appraisal support grounded in South Australian market knowledge. The team draws on current comparable data across Adelaide suburbs to give you a rent figure you can act on with confidence. For landlords managing multiple properties or planning portfolio growth, HOSO's property management services cover the full scope of rental strategy, compliance, and tenant management. Local expertise, clear reporting, and a focus on long-term asset performance are what set HOSO apart from generalist agencies.

FAQ

What is a rental appraisal?

A rental appraisal is a professional assessment of the weekly rent a property can achieve in the current market, based on comparable properties, local demand, and the property's specific features.

How much does a rental appraisal cost in Australia?

A standard rental appraisal typically costs $200–$400 and is valid for 60–90 days. Full narrative appraisals cost more and are generally required for mortgage or refinancing applications.

How often should I get a rental appraisal?

Landlords should commission a rental appraisal at least once every 12 months. Markets shift, and an outdated figure can result in lost income or extended vacancy at lease renewal.

What documents should I bring to a rental appraisal?

Bring your current lease, rent roll, and recent payment records. Providing this documentation gives the appraiser stronger evidence and produces a more accurate, defensible rent figure.

Do lenders use the rent in my lease for financing decisions?

Lenders commonly disregard the actual lease rent and instead rely on an independent market rent figure. A credible appraisal report is required for any refinancing or new lending application.