Tenant screening is the process landlords use to evaluate rental applicants across credit history, eviction records, criminal background, income verification, and prior rental conduct before signing a lease. For South Australian landlords, this process is the single most reliable method for separating financially stable, low-risk tenants from applicants whose history predicts costly problems. Understanding why tenant screening is important goes beyond gut instinct. It converts subjective impressions into documented, criteria-based decisions that protect your property, your income, and your legal standing under the Residential Tenancies Act 1995 (SA).

Why tenant screening is important for reducing landlord risk

Tenant screening reports combine financial history, background checks, and rental records to give landlords a complete picture of an applicant's reliability. No single data point tells the full story. A tenant with a reasonable credit score may carry an undisclosed eviction from a Prospect rental two years ago, or a history of property damage that never reached a credit bureau. Screening closes those gaps systematically.

The financial stakes are direct. An eviction in South Australia typically costs a landlord between $5,000 and $15,000 once you account for legal fees, SACAT filing costs, lost rent during the vacancy, and re-leasing expenses. That figure does not include property damage beyond the bond. Screening is not a bureaucratic formality. It is the most cost-effective risk management tool available to any landlord in the Adelaide market.

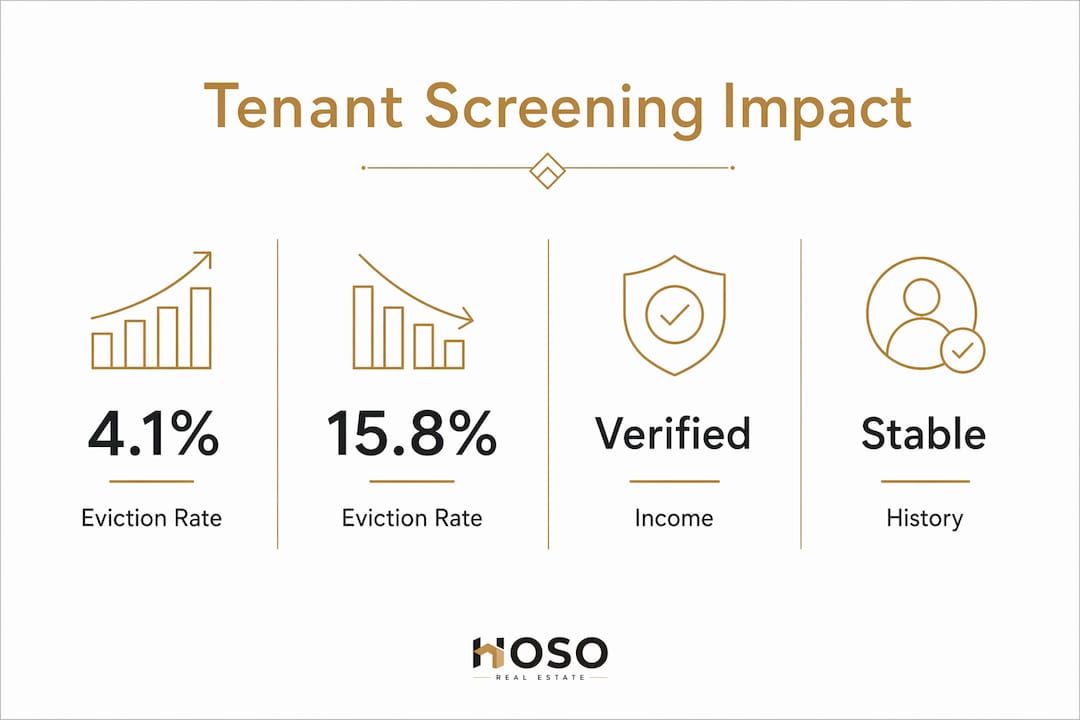

Screened tenants show a 4.1% eviction rate compared to 15.8% for unscreened tenants. That gap represents a nearly fourfold reduction in eviction risk, which translates directly into fewer SACAT appearances, fewer vacancy periods, and more predictable rental income across your portfolio.

What does the tenant screening process include?

A thorough screening process covers five distinct areas. Each serves a different purpose, and omitting any one of them creates a blind spot.

- Credit report analysis. A credit report reveals payment history, outstanding debts, defaults, and court judgements. It predicts whether a tenant will pay rent on time. However, credit reports have a known limitation. Approximately 28% of eviction filings never generate a credit entry, meaning a tenant with a clean credit file may still carry a prior eviction that simply was not reported to a bureau.

- Dedicated eviction history search. Because eviction filings are often invisible on credit reports, a separate eviction database search is non-negotiable. This captures filed-but-dismissed cases, settled disputes, and tribunal orders that credit bureaus do not record.

- Criminal background check. This check identifies convictions relevant to tenancy risk. Landlords must apply this check consistently and avoid blanket denials based on arrest records alone, in line with fair-housing principles discussed further below.

- Income verification. Confirming that an applicant earns sufficient income to sustain rent payments is fundamental. The standard benchmark is gross income of at least three times the weekly rent. Document-based verification, such as reviewing pay stubs, detects only 40 to 50% of fraudulent income claims. Payroll database verification lifts that detection rate to 85 to 95%, making it the more reliable method.

- Rental history and references. Direct contact with previous landlords or property managers reveals conduct that no database captures: noise complaints, lease breaches, maintenance neglect, and departure condition. A tenant who left a Glenelg property in poor condition will not disclose that voluntarily.

Pro Tip: When contacting previous landlords, ask two specific questions: "Would you rent to this person again?" and "Did they give proper notice at the end of the tenancy?" Vague or hesitant answers to either question are as informative as a direct negative response.

How does tenant screening reduce financial risks and vacancies?

The financial case for screening is grounded in turnover cost data, not theory. Every time a tenancy ends prematurely, a South Australian landlord faces advertising costs, property condition reports, potential maintenance between tenancies, and a vacancy period that averages two to four weeks in most Adelaide suburbs. In higher-demand areas like Norwood, Unley, or Burnside, that vacancy may be shorter, but the re-leasing cost remains.

| Risk factor | Without screening | With screening |

|---|---|---|

| Eviction rate | 15.8% | 4.1% |

| Income fraud detection | 40 to 50% | 85 to 95% |

| Eviction filings missed | Up to 28% of cases | Near zero with dedicated search |

| Average tenancy length | Shorter, higher turnover | Longer, lower turnover |

Verified income is the strongest predictor of tenancy stability. A tenant whose income is confirmed through a payroll database, rather than a self-submitted pay stub, is far less likely to fall into arrears in month three. Over 84% of landlords encounter falsified income documents, and 73% of those cases are only detected after the tenant has moved in. By that point, the landlord is managing arrears, not preventing them.

Stable rental history compounds the benefit. A tenant with two or three consecutive tenancies of 12 months or more, each ending without dispute, is statistically more likely to renew and maintain the property. Screening identifies that pattern before the lease is signed, not after the first breach notice is issued.

What legal and compliance considerations should SA landlords know?

Tenant screening in South Australia operates within a framework of privacy law, anti-discrimination obligations, and tenancy regulation. Getting the process wrong exposes landlords to complaints, penalties, and SACAT proceedings.

- Privacy and consent. Under the Privacy Act 1988 (Cth), landlords must obtain explicit written consent from applicants before accessing their personal information for screening purposes. Consent embedded in a general application form is insufficient. Standalone written disclosure is required before any report is pulled.

- Anti-discrimination obligations. The Equal Opportunity Act 1984 (SA) prohibits discrimination on the basis of race, sex, age, disability, and other protected attributes. Screening criteria must be applied uniformly to every applicant. Inconsistent application of criteria creates legal exposure even when the underlying decision was commercially reasonable.

- Criminal history assessments. HUD guidance advises against blanket criminal history bans and recommends individualised assessments that consider the nature of the offence, time elapsed, and evidence of rehabilitation. While HUD guidance is a US standard, the underlying principle aligns with SA anti-discrimination law. Denying an applicant solely on the basis of an arrest record, without a conviction, is not a defensible position.

- Adverse action disclosure. When a landlord declines an applicant based on screening results, the applicant has a right to know the general basis for that decision. Documenting the reason with reference to your stated screening criteria is the correct practice.

- SACAT relevance. The South Australian Civil and Administrative Tribunal handles tenancy disputes, including those arising from improper screening practices or discriminatory conduct. Maintaining clear, consistent records of your screening criteria and decisions is your primary protection if a complaint is lodged.

Common pitfalls and how to avoid them

Most screening failures come from process gaps, not bad intentions. These are the most common errors Adelaide landlords make, and the practical fixes for each.

- Relying solely on credit scores. A credit score is a snapshot of financial behaviour, not a complete tenancy risk profile. Post-2025, FICO scores are inflated by the removal of medical debt from credit reporting and authorised-user additions. Rental-specific scores such as ResidentScore® predict eviction 15% more accurately than standard FICO scores for this reason. Use a rental-specific score where available.

- Skipping the eviction search. Many landlords pull a credit report and assume it covers eviction history. It does not. A dedicated eviction database search is a separate step and a necessary one.

- Accepting documents at face value. Pay stubs, bank statements, and employment letters are the most commonly falsified documents in rental applications. Payroll database verification, where the income is confirmed directly from the employer's payroll system, removes the opportunity for document manipulation entirely.

- Applying criteria inconsistently. Screening criteria must be documented in writing before applications open, then applied identically to every applicant. Deviating from stated criteria, even informally, creates discrimination risk and weakens your position in any subsequent dispute.

- Failing to check references directly. Email-based reference checks are easy to fabricate. A direct phone call to the previous property manager or landlord, using a number sourced independently rather than one supplied by the applicant, is the only reliable method.

Pro Tip: Build a one-page screening checklist that lists every criterion and the minimum threshold for each. Date and sign it before advertising the property. This document becomes your evidence of consistent, non-discriminatory practice if any applicant challenges your decision.

For a broader view of how professional oversight reduces landlord risk, the article on property management protecting landlords covers the full scope of risk management beyond the screening stage.

Key takeaways

Thorough tenant screening reduces eviction rates, detects income fraud, and protects landlords from legal exposure by replacing subjective assessment with documented, criteria-based evaluation.

| Point | Details |

|---|---|

| Screening cuts eviction risk | Screened tenants have a 4.1% eviction rate versus 15.8% for unscreened tenants. |

| Credit reports miss eviction history | Up to 28% of eviction filings never appear on credit reports; a separate search is required. |

| Income fraud is widespread | Over 84% of landlords encounter falsified income documents; payroll database checks detect up to 95% of fraud. |

| Compliance is non-negotiable | SA landlords must obtain standalone written consent and apply criteria uniformly to avoid discrimination complaints. |

| Documented criteria protect landlords | A written screening checklist applied consistently is your primary defence in any SACAT dispute. |

The screening standard Adelaide landlords cannot afford to ignore

From our experience managing properties across Adelaide's inner suburbs and growth corridors, the landlords who face the most costly tenancy problems share one trait: they made a leasing decision based on a good impression rather than verified data. A well-presented applicant with a plausible story and a passable credit score is not the same as a verified, low-risk tenant.

The screening environment in 2026 is more complex than it was five years ago. Document fraud has become more sophisticated. Credit scores are less reliable as a standalone indicator following changes to medical debt reporting. And the cost of a failed tenancy, measured in SACAT time, vacancy loss, and property damage, has increased with rising property values across suburbs like Norwood, Prospect, and Mitcham.

What we have found is that landlords who treat screening as a one-time document collection exercise miss the most important signals. The eviction history that does not appear on a credit report. The income figure that looks right on paper but cannot be verified through a payroll system. The previous landlord reference that was never actually called. These are the gaps that turn a promising application into a six-month dispute.

Screening is not about distrust. It is about applying the same standard of due diligence to a tenancy decision that you would apply to any other financial commitment of comparable size. Your property is an asset. The tenant you place in it will determine its condition, its income consistency, and its long-term value. That decision deserves a process, not a gut feeling.

— HOSO

How HOSO Real Estate supports landlords with tenant screening

HOSO Real Estate manages the full tenant screening and leasing process for landlords across Adelaide, from application assessment and income verification to reference checks and compliance documentation.

Our property management services cover every stage of the tenancy lifecycle, including structured screening protocols that align with SA tenancy law and anti-discrimination obligations. Landlords working with HOSO benefit from consistent, documented screening criteria applied to every application, reducing both tenancy risk and legal exposure. Whether you manage a single investment property in Unley or a portfolio across multiple Adelaide suburbs, HOSO Real Estate provides the professional oversight your investment requires. Visit HOSO Real Estate to learn more about how we protect landlord interests from the first application to lease renewal.

FAQ

What is tenant screening and why does it matter?

Tenant screening is a structured evaluation of a rental applicant's credit history, eviction records, criminal background, income, and rental conduct. It matters because screened tenants have a 4.1% eviction rate compared to 15.8% for unscreened tenants, representing a direct reduction in financial risk.

Does a credit check cover eviction history?

No. Approximately 28% of eviction filings never appear on a credit report, so a dedicated eviction database search is required as a separate step in the screening process.

What are SA landlords' legal obligations when screening tenants?

SA landlords must obtain standalone written consent before accessing applicant information, apply screening criteria uniformly to avoid breaching the Equal Opportunity Act 1984 (SA), and document the basis for any adverse decision. SACAT can hear complaints arising from discriminatory or improper screening conduct.

How can landlords verify income reliably?

Payroll database verification confirms income directly from an employer's payroll system and detects 85 to 95% of fraudulent income claims, compared to 40 to 50% detection through document review alone.

How much does a tenant screening report cost?

Standard screening reports range from $30 to $50 per applicant. Reusable reports, where the applicant pays once and shares access with multiple landlords, cost around $60 and reduce the administrative burden for both parties.